One of the questions I get most often is: “why isn’t the portfolio simply all-in on the obvious winners?”

One of the questions I get most often is: “why isn’t the portfolio simply all-in on the obvious winners?”

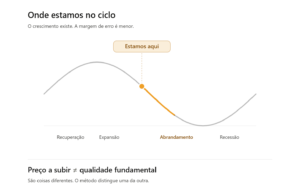

The answer lies in regime reading.

Recent data is sending mixed signals. US manufacturing PMI has risen to multi-year highs. But much of that move appears to come from inventory restocking and higher costs — not robust final demand. At the same time, leading indicators remain fragile, employment is showing cracks, and implied volatility stays elevated.

My reading: this is not a clean Expansion. It’s a transition phase, where growth exists but the margin for error is smaller.

What this means in practice for how I manage the portfolio:

→ I maintain structural exposure to AI, semiconductors, and digital infrastructure. The engine doesn’t get dismantled in a transition phase.

→ But I prioritise quality within the theme. In periods of uncertainty, the difference between companies with solid fundamentals and companies that are only rising on momentum becomes decisive.

→ And I reinforce the buffers: greater defensive weight, some protection, and concentration discipline in names that have grown too large.

The takeaway: in a transition regime, the most expensive mistake isn’t being underexposed to growth. It’s confusing price going up with fundamental quality. They are different things — and the market tends to teach that lesson in the hardest way.

Method above momentum. Always.

#investing #AI #semiconductors #macro